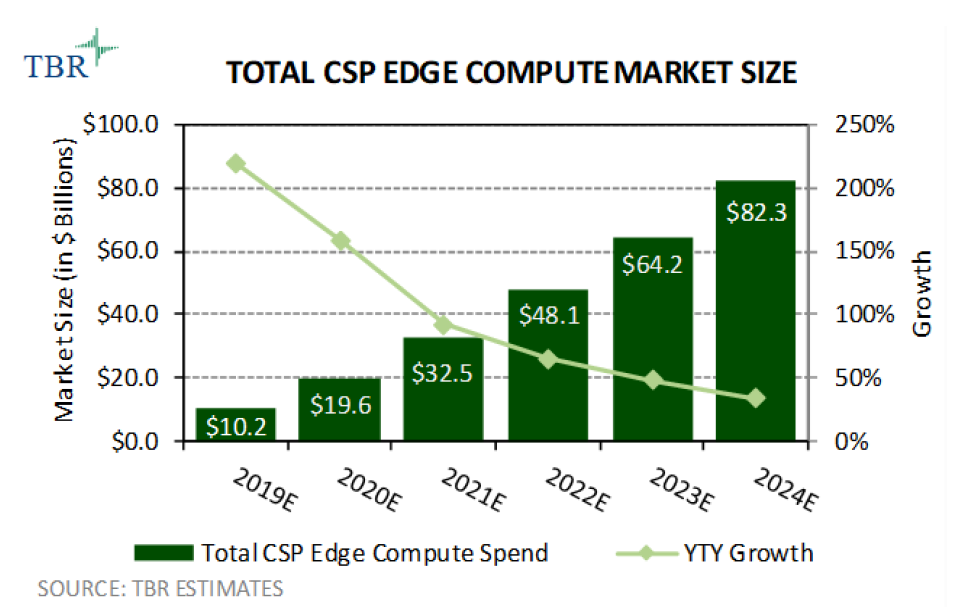

TBR estimates over 1.2 million network sites and cell sites will become mini data center (edge) locations globally by 2025, up from nearly 9,000 sites globally at the end of 2019.

The primary driver of edge build-outs during the forecast period is CSPs’ network transformations, which entail migrating to a cloudified and virtualized network, and webscales’ edge initiatives to support their cloud businesses and digital lifestyle endeavors.

In this new architecture, network functions will be virtualized and housed in NFVI, which is essentially a data center. Network sites, such as central offices, have been the primary edge compute location to date, with cell site builds expected to ramp up significantly in 2021 and become the primary location for the CSP edge by 2025.

2019~2024 CAGR 51.8%

OMDIA 咨询公司的研究认为,到 2027 年全球企业边缘计算服务的市场规模将达到 2,450 亿美元,对比 2023 年的 1,162 亿美元翻一番还多。2023-2027 期间的年复合增长率(CAGR)为 22.8%。

从服务提供商角度,来自 Hyperscales(大型云基础设施服务商)和电信运营商的份额会增加,而系统集成和企业信息化咨询公司的份额会减少。

从行业分布角度,制造业仍是领先行业,金融服务、零售、交通运输和政府会紧跟其后。

OMDIA 针对全球运营商 5G 消费者业务的资费合约跟踪数据显示,50GB 及以下的套餐占比从 5G 初期的 40% 提升到了 56%。

OMDIA 认为原因是很多运营商的子品牌,或者 MVNO 提供了更小流量尺寸的选择。甚至一些运营商直接用 4G 的资费套餐用于 5G 用户(如果当地 5G 网络覆盖还不够好的话)。

Unlimited 不限量套餐的占比保持在 23% 左右。但需注意,以美国运营商为代表的,所谓 Unlimited 其实是超过额度要限速的。

每一代网络技术都会带来一轮技术红利。运营商适当控制住流量释放的节奏(从价格角度,而不是很低价的倾销),对于 5G 商业变现很重要。

新冠疫情导致的 Lockdown 对麦当劳产生了剧烈冲击。

从最新数据看,麦当劳(美国)的门店销售已经恢复到疫情前的增长状态。麦当劳的股价也回到了疫情前状态。

如扣除疫情期间部分,可看到近年来麦当劳的门店销售一直在保持在 5% 以下的增长,虽然不高,但待续。